How to Check Your Credit Score

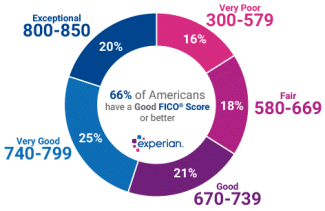

What is a good credit score?

Credit Reports

Part of our mission at Love Your Finances is to help you and our clients gain access to opportunities that can improve your quality of life and your personal finances. My team and I do this by providing the most complete and multidimensional financial information available to help our customers make the best possible choices.

We value our reader's success as much as our own. That’s why we go beyond credit data to offer the insights businesses and consumers need to make informed decisions and achieve great things. We believe that if you keep building on good choices, you’ll continue to create solid opportunities.

So why then the hype regarding credit reports? These reports provide important information about your payment history on bills, loans, current debt, and other financial information. The report shows your place of work, where you reside, and if you’ve been sued, arrested, or even filed for bankruptcy.

Credit reports also assist lenders in deciding whether to extend credit to you or whether to approve a loan. The interest rate you will be charged will be determined by the information on the credit report. It is also not uncommon for employers, insurers, and rental property agents to assess your credit score based on the report.

I would certainly encourage you to check your credit report on a regular basis to ensure that your personal and financial information is being accurately reported and that no fraudulent activity shows up on the report. If you should find errors on your credit report, it is easy enough to have these corrected.

Credit Scores

What’s the big deal when it comes to credit scores anyway? Well, a credit score is a summary of your credit history expressed as a number ranging from 300 to 850. These numbers rate your credit risk and can assist creditors in determining whether to give you credit. It also assists them in deciding the terms you are offered and the rate you will pay. Having a high credit score can benefit you in many ways and makes it easier for you to obtain loans, rent a house and lower your insurance rate.

The credit score model is a risk-based system that calculates the possibility of you defaulting on your next loan — so, the lower your score, the higher the possibility of you defaulting.

What impacts your credit score?

Suffice it to say that being late on payments or defaulting on loans is guaranteed to lower your credit score.

Other ways in which you can tarnish your credit score:

- By applying for multiple credit cards or loans.

- Letting your credit card balance get too high

- Closing credit cards – the amount of credit available to you goes down.

- Renting a car without a credit card

- Not paying parking tickets or medical bills. Those bills don’t just pay themselves and after a while, these bills get sent to collection agencies which is reflected on your credit report.

- A new phone contract – phone companies pull a hard credit check when you sign up, causing your credit score to take a bit of a dip.

What are the credit score tiers and ranges?

Identifying your credit score range can be quite difficult. This is because financial institutions determine ranges differently. As a result, with one bank, your credit score could place you in their “excellent” bracket, while the same score might place you in the “good” range with a different bank.

Generally speaking, if you can keep your score above 670 you will be considered a lower risk and if you can get it in the mid-700s then you will almost have lenders asking to loan you money since they know you are a pretty safe bet. The higher your score the more you can negotiate rates on loans, etc. as well.

Credit Freeze

In this technological era and the ease at which data is accessible, you can obtain a credit freeze to restrict access to your credit report in the event of a data breach or identity theft. You have the right to place or lift a credit freeze for free and you can place a freeze on your own credit files and on those of your children age 16 or younger. An important point to note is that a credit freeze does not expire and until it is lifted by you, it stays in effect.

Should you want to lift a credit freeze in order to give lenders access to your credit history, you can contact each credit reporting agency and request them to lift the freeze. It takes about an hour if requested by telephone or three business days if requested by mail.

Can I check my credit score for free?

Free Credit Reports

Don’t we all enjoy the free things in life – I know I certainly do! So, it is a rather nice gesture that once a year a free credit report from each of the three credit reporting agencies, namely Equifax, Experian and TransUnion is made available to you. Even better is that you can request all three reports at once or at different intervals during the year. Just a note to keep in mind – you won’t be able to see your actual credit score, but this is available for a small fee.

You can access your credit report here.

How can I check my credit score without hurting my credit?

Checking your credit is savvy

If you’re on top of your credit score, you can quickly be alerted if something is wrong – such as identity theft or fraud.

Be proactive before applying for credit. It makes sense to have an idea of what the lender will see when assessing your application and your credit score. Knowing your credit score can keep you from needlessly losing points by applying for products you won’t qualify for.

Either way, you’ll see an “inquiry” on your credit report. It means that someone, either you or a lender has pulled your credit report. If you have applied for credit, you’re likely to see the lenders or card issuers listed on your report. You may also see collection agencies, lenders to whom you have not applied, and records of when you checked your own credit.

Hard vs. soft inquiries

The terminology regarding credit reports is quite interesting:

Hard Inquiries

Also referred to as hard pulls are the types of inquiries that can cost you points. This happens when your credit report is pulled for the purpose of deciding whether to extend credit or additional credit to you.

- These hard inquiries may cost up to five points and should not happen without your knowledge or your consent.

- A hard inquiry stays on your credit report for two years, but any effect on your credit score fades sooner than that.

Soft Inquiries

These inquiries have no effect on your credit score.

A soft inquiry or soft pull occurs when you or a creditor is looking to preapprove you for a loan or credit card.

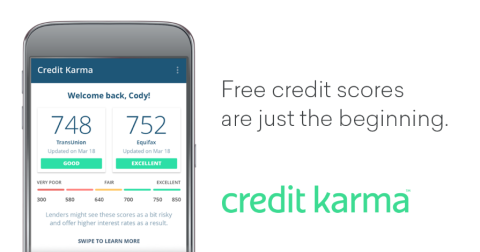

Free Credit Scores

The two places I like to check my credit score, history, etc. are Credit Karma and WalletHub. Both are free but do require you to register with them. You can even set up alerts within them so you will be emailed when any significant changes happen to your credit.

Is it bad to check your credit score on credit karma?

Debunking credit myths

As of December 2017, the Huffington Post noted in a recent survey that many consumers are still confused about credit scores and it seems it’s just something we can’t get right, and this confusion can have a massive impact on our financial future.

So, what are the popular myths then?

Myth 1: You have just one credit score.

This is a tough myth to bust and the reality is that you have many, many credit scores. In the popular FICO model, there are 49 different scores and the score that you pay for usually isn’t the one a potential lender sees.

Depending on the type of inquiry being made such as an automotive lender vs a mortgage lender, credit scores can vary quite significantly according to what credit bureau data is being used (Equifax, Experian, or TransUnion) and which model is used i.e. FICO, Vantagescore or another model. The light at the end of the tunnel is that your various credit scores are connected, and this means if your credit is rated as ‘’good’’ in one model, then it should be ‘’good’’ in all models.

Myth 2: Checking your own credit hurts your score.

Don’t believe everything you read – when you request your own credit score, this is deemed a soft inquiry and does not affect your credit whatsoever. These soft inquiries are not used for making lending decisions – remember, that is a hard inquiry.

Being in control of your credit score report is a good thing as it gives you an idea of where you stand and how your actions affect your credit rating. So, bottom line, don’t be afraid to check your credit score – it does no harm in the slightest.

Myth 3: Closing your oldest credit card will hurt your score.

Oh, how we love to hold onto antiquated beliefs! Look, closing your oldest credit card account is not going to magically remove that card history from your credit report and shorten your credit age. Whether accounts are open or closed, they remain on your credit report and continue to age just like any other account.

After a period of ten years, credit bureaus remove closed accounts from your reports, so you won’t get the benefit of a long, on-time payment history of a closed account forever. It is good practice to keep your oldest card open, even if you don’t use it, to help with your overall credit age. From time to time put a small purchase on it to keep it active otherwise some credit card companies will cancel the card without even telling you.

Before deciding to close a credit card account, ensure your other credit card balances are low enough to compensate. The reason is, that if your oldest credit card account has a large limit, it could be contributing to one of the most important factors of your credit score – your credit card utilization rate. This rate is your total credit card balances divided by your total credit card limits and it generally indicates how much you rely on credit. Closing an account with a high limit could inflate your credit card utilization.

I hope you’ve enjoyed reading about how easy it is to access and maintain your credit scores. Credit is one of those facets that not many of us can live without, so we must ensure we take the right steps to guarantee good credit ratings.

Thank you for reading!

Cheers

Derek Notman